In the May 2018 Nonprofit Connection, we discussed ways to safeguard cash and other assets at special events. The following article discusses other important items to consider in planning special events.

Quid Pro Quo

Quid pro quo in relation to special events is a payment of more than $75 that a donor makes to a charity that is part contribution and part purchase of goods or services. The best example of this is the purchase of a dinner ticket. A donor pays $100 for a ticket but the dinner is valued at $30. The tax deductible contribution part of the ticket is $70. This is considered a quid pro quo contribution.

The organization must provide the donor a disclosure statement because the donor’s payment is more than $75. Usually this statement is included on the dinner ticket. Although the deductible contribution is only $70, disclosure is required because the full payment made is more than $75. IRS imposes a penalty on an organization if this disclosure is not made. The penalty is $10 per contribution, not to exceed $5,000 per fundraising event or mailing.

Auction Items

It is important to develop a method for tracking auction items as they are collected. An inventory list can guard against theft of auction items, provide good records for sending donor acknowledgement letters, and provide a history of donors for future fundraising events. The list should include the following: item description, item value (if supplied by the donor), who gave the item, and who received the item. After the event, update the list with the amount received for each item during the auction. Proceeds on the list should be reconciled to the accounting records.

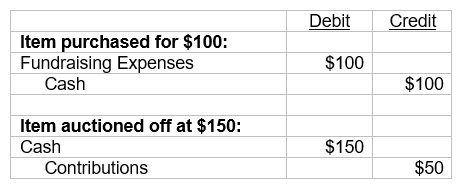

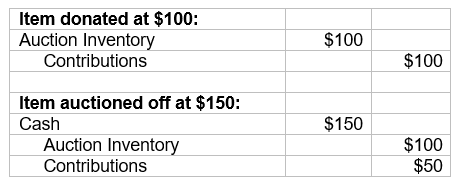

Accounting for auction items is commonly done incorrectly. This is the proper accounting for auction items under two different scenarios.

Scenario #1: Item was purchased by the organization.

Scenario #2: Item was donated to the organization for auction.

Scenario #2 is the preferred method for recording items donated for auction. Consider the size of your auction and how long items are held before deciding to switch to this method.

Raffles

Requirements for raffles vary by state. During the planning phase of your event, you should gather information on the license requirements, the types of raffles allowed, and who can participate. The license requirements for Wisconsin and Minnesota are as follows.

In Wisconsin, any organization conducting a raffle must obtain a license through the Division of Gaming’s Office of Charitable Gaming. There are two types of licenses – Class A and Class B. The Class A raffle license is needed when tickets are sold in advance and the day of the raffle. The Class B raffle license is needed when tickets are only sold the day of the raffle. Bucket raffles and 50/50 raffles are common examples of a Class B raffle. An organization conducting both Class A and Class B raffles must obtain both license types. Applications and more information can found at: https://doa.wi.gov/Pages/LicensesHearings/RaffleLicense.aspx.

In Minnesota, an exemption from gambling activity such as raffles may be obtained from the Minnesota Gambling Control Board if the organization qualifies. An exempt permit is required when the following applies: 1) the total value of all prizes donated and purchased is less than $50,000 for the year, and 2) gambling activity is limited to five days during the year. An application for the exempt permit must be filed for each year. Organizations that don’t meet these two requirements must obtain a lawful gambling license. Applications and more information can found at: https://mn.gov/gcb/raffles.html.

There are also federal requirements regarding raffles. If the organization generated over $15,000 in raffle and other gambling proceeds, it must complete Part III of Form 990, Schedule G. Revenue and expenses related to the raffles or other gambling activities are reported on this schedule. If a single donated prize is valued at more than $5,000, it must be reported on Schedule B of Form 990. Prize winners of cash or gifts valued at over $600 should be issued a 1099-MISC (included in Box 3). Also, winners from wagering activities that receive winnings over $600 should be issued a Form W-2G.

Other Items

Lastly, consider these other items when planning your next event:

- Creating a budget for event expenses

- Obtaining event insurance

- Obtaining a liquor license or event permit, if either are applicable

- Training volunteers before the event

- Reconciling revenue and expenses to supporting schedules and auction inventory listing

- Scheduling a debriefing meeting shortly after the event to discuss and make note of possible improvements